Story map

Green ammonia serves as the leading zero-carbon fuel for global energy shipping because it stores and transports far more easily than pure hydrogen. The market already generates USD 676.8 million in annual revenue this year and scales quickly. Production plants, port infrastructure and export corridors now attract targeted government incentives and long-term contracts.

Start here

The short version

- 01Green ammonia turns renewable hydrogen into a practical shipping fuel that liquefies at far higher temperatures than pure hydrogen. The market reaches USD 676.8 million in revenue this year and grows rapidly toward 2033. EU FuelEU Maritime rules and US tax credits already channel

- 02Pure hydrogen requires cryogenic temperatures of minus 253 degrees Celsius or extreme pressure.

- 03The US Inflation Reduction Act offers up to three dollars per kilogram for clean hydrogen used in ammonia production.

Method, source and disclosure

This analysis is prepared by the Market Lens desk from the sources named in the story and publicly available market information. Material revisions appear in the updated timestamp.

View primary source ↗Why Green Ammonia Beats Pure Hydrogen for Shipping

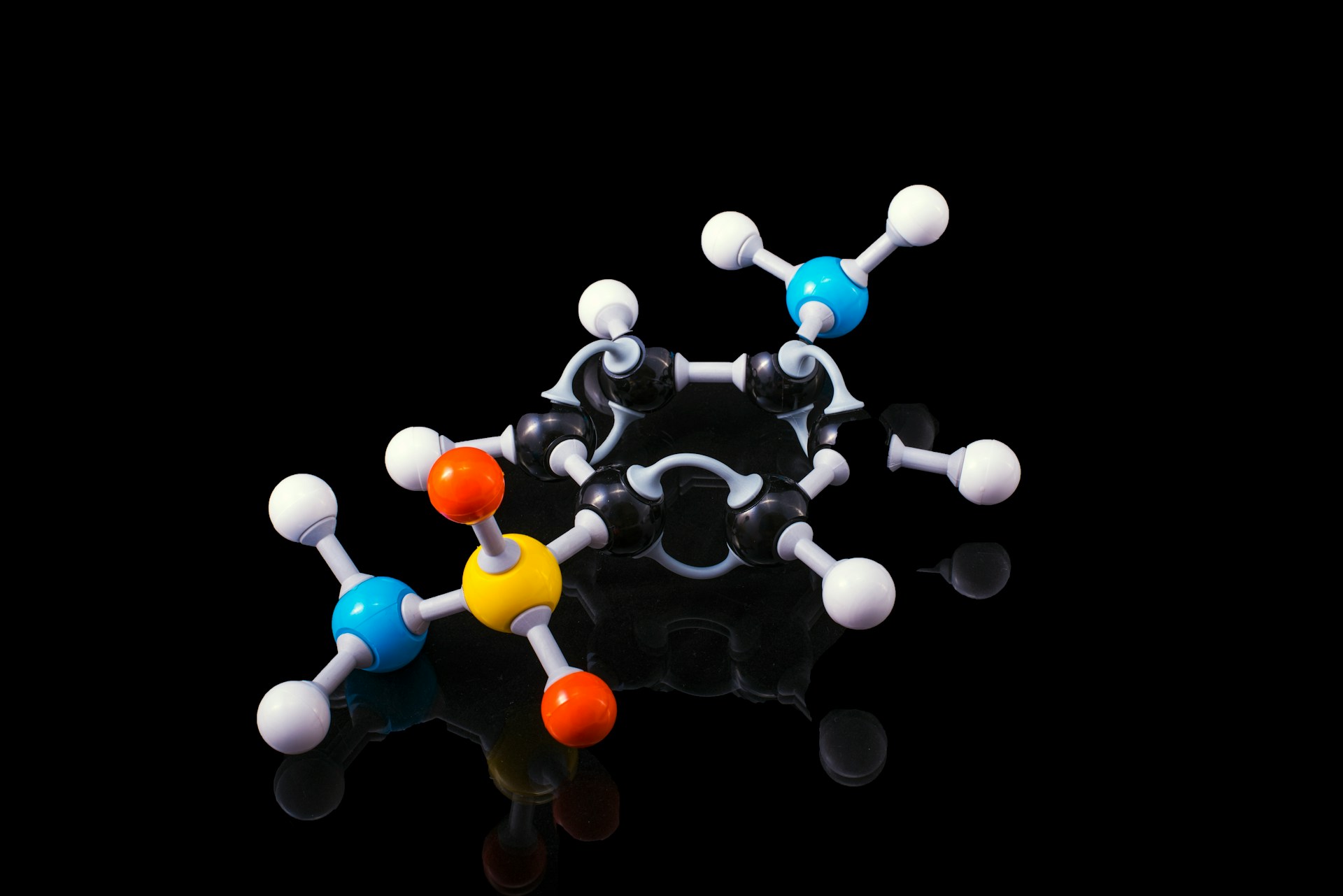

Pure hydrogen requires cryogenic temperatures of minus 253 degrees Celsius or extreme pressure. Green ammonia liquefies at minus 33 degrees Celsius or modest pressure of about 10 bar. This difference makes ammonia practical for large tankers and existing port systems.

Ammonia carries hydrogen in a stable chemical form without losing energy during long voyages. Combustion or fuel-cell use releases only nitrogen and water. The same molecule already moves safely around the world as fertilizer feedstock.

Early studies confirm ammonia-powered vessels can reach cost parity on select routes by 2026 when subsidies apply. South Africa-Europe iron-ore corridors show full decarbonisation possible by 2035 with local green ammonia supply. Ports now plan dedicated bunkering hubs to support these routes.

Government ESG Tax Credits Fuel Infrastructure

The US Inflation Reduction Act offers up to three dollars per kilogram for clean hydrogen used in ammonia production. Credits tier by carbon intensity and reward projects that meet wage and apprenticeship rules. These incentives lower the capital cost of electrolysers and Haber-Bosch plants.

European programmes and national subsidies in India, Australia and Morocco match the US approach. Morocco recently advanced a 4.5-billion-dollar green ammonia project in Laayoune. Australia and Oman host gigawatt-scale renewable hubs that feed ammonia output.

Tax credits de-risk the first wave of infrastructure. Developers combine them with green bonds and multilateral loans. The result appears in faster final investment decisions for plants targeting 2028-2030 operations.

Maritime Decarbonization Mandates Drive Demand

EU FuelEU Maritime rules took effect in January 2025 and cut the greenhouse-gas intensity of ship fuel each year. Vessels calling at EU ports must meet annual averages or buy compliance units. This creates immediate demand for low-carbon ammonia and other zero-emission fuels.

The International Maritime Organization targets net-zero shipping by 2050 and keeps ammonia on its approved fuel list. A one-year delay in the global carbon-pricing framework slowed some projects yet left regional mandates intact. Shipowners now order dual-fuel vessels that run on ammonia or methanol.

Mandates push ports to install ammonia storage and handling systems. Early adopters gain competitive advantage through lower compliance costs. The combination of FuelEU penalties and IMO goals turns regulatory pressure into infrastructure investment signals.

| Fuel Option | Liquefaction Temperature | Storage Pressure | Existing Infrastructure Fit | Zero-Carbon Status |

|---|---|---|---|---|

| Pure Hydrogen | -253 °C | Very high | Poor | Yes |

| Green Ammonia | -33 °C | Moderate | Strong | Yes |

| Green Methanol | -97 °C | Moderate | Good | Yes |

The table shows why ammonia leads among zero-carbon options for long-distance shipping. Existing tanker fleets and port terminals require only modest upgrades. This compatibility accelerates infrastructure rollout.

Chemical Engineering Companies Build the Plants

Yara International, CF Industries and Air Products lead green ammonia production through partnerships with electrolyser makers. Thyssenkrupp Uhde supplies the core Haber-Bosch technology adapted for renewable hydrogen. These firms convert engineering expertise into turnkey plants that scale from pilot to gigawatt levels.

NEOM in Saudi Arabia targets commercial start-up in 2026 with 1.2 million tonnes of annual capacity. Indian developer AM Green builds a one-million-tonne facility in Kakinada backed by European offtakers. Chemical engineers optimise renewable power integration to keep production costs competitive.

Engineering contractors also design port terminals and ship fuel systems. Their role extends beyond construction to safety standards and crew training. This full-chain capability shortens the time from financing to first cargo.

Long-Term Export Contracts Secure Finance

Uniper signed a binding deal in January 2026 for up to 500,000 tonnes per year of renewable ammonia from India starting in 2028. Air Products and Yara advance ownership talks for US and Saudi projects worth several billion dollars. These contracts guarantee revenue streams that support debt financing and equity raises.

Buyers include European utilities, fertilizer makers and shipping lines seeking fuel security. Sellers lock in prices linked to renewable power costs plus a margin. The structure mirrors traditional LNG deals yet adds green certification for regulatory compliance.

Long-term agreements reduce investor risk and unlock export infrastructure loans. Ports in Australia, Oman and Morocco now plan dedicated loading terminals. The contracts also signal demand volumes that justify larger electrolyser orders and grid upgrades.

Monitor signed offtake deals and IMO regulatory updates through 2026. These milestones reveal which corridors and technologies will capture the next wave of infrastructure capital. Early visibility here guides decisions on project scale and location.